For many homeowners, flood insurance might not be the first thing on their minds, especially if they don’t live in areas traditionally known for flooding. However, recent data from the Natural Resources Defense Council (NRDC) suggests that reevaluating this stance is crucial. With the rising risks of flooding, even those outside known flood zones should seriously consider the implications of not having flood insurance.

The Surprising Reality of Flood Risks

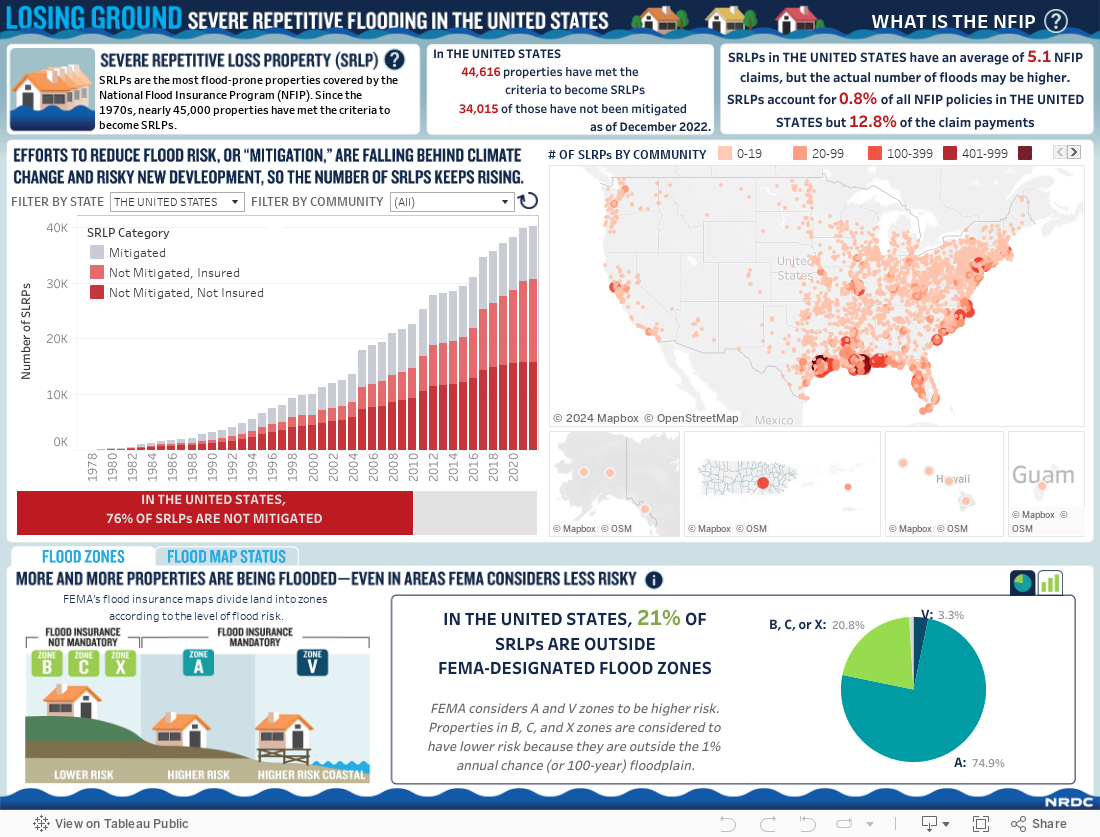

The NRDC’s findings reveal a concerning trend: less than 1% of homes covered by the National Flood Insurance Program (NFIP) are categorized as severe repetitive loss properties (SRLPs), yet they astonishingly account for over 10% of all NFIP claims. This statistic is a stark reminder that flood damage can be both financially and emotionally devastating, and it’s not just confined to high-risk areas.

What Are Severe Repetitive Loss Properties?

SRLPs are homes that have experienced significant flood damage on multiple occasions. They are classified into two categories:

- Definition A: Homes with four or more separate claim payments exceeding $5,000 each.

- Definition B: Homes with two or more claims where the total exceeds the property’s value.

The number of these properties has increased by nearly 20% since 2020, signaling a growing flood risk.

Floods Don’t Respect Maps

One of the most eye-opening aspects of the NRDC’s report is that about 20% of SRLPs are located outside FEMA-designated flood zones. This means that even areas not traditionally seen as flood-prone are experiencing significant flood events. States like Texas and Tennessee, for instance, are seeing an increase in flood incidents in areas not previously identified as high risk.

The Implications for Homeowners

If you’ve never considered flood insurance because you’re not in a known flood zone, it might be time to rethink that decision. The changing climate and evolving environmental factors are making floods more common and unpredictable. Moreover, the majority of SRLPs have not received mitigation assistance, and many homeowners in these areas are dropping flood coverage, potentially leaving them vulnerable to financial loss.

The Call to Action

This situation is a wake-up call for homeowners. Flood insurance should be a key consideration in your overall home protection strategy, regardless of your current flood risk perception. It’s about being proactive rather than reactive in the face of potential natural disasters. Using insurance carrier resources, a risk advisor can help you assess your need for flood coverage.

Conclusion

The rising number of severe repetitive loss properties is a clear indicator that flood risks are changing. As a homeowner, staying informed and considering flood insurance, even if you think you’re in a safe area, could be one of the most important decisions you make for the protection of your home and financial future.